There are so many reasons why people choose to use online payday loans, this’s because payday loans do have their place, and can’t really be avoided, especially in situations that are exigent.

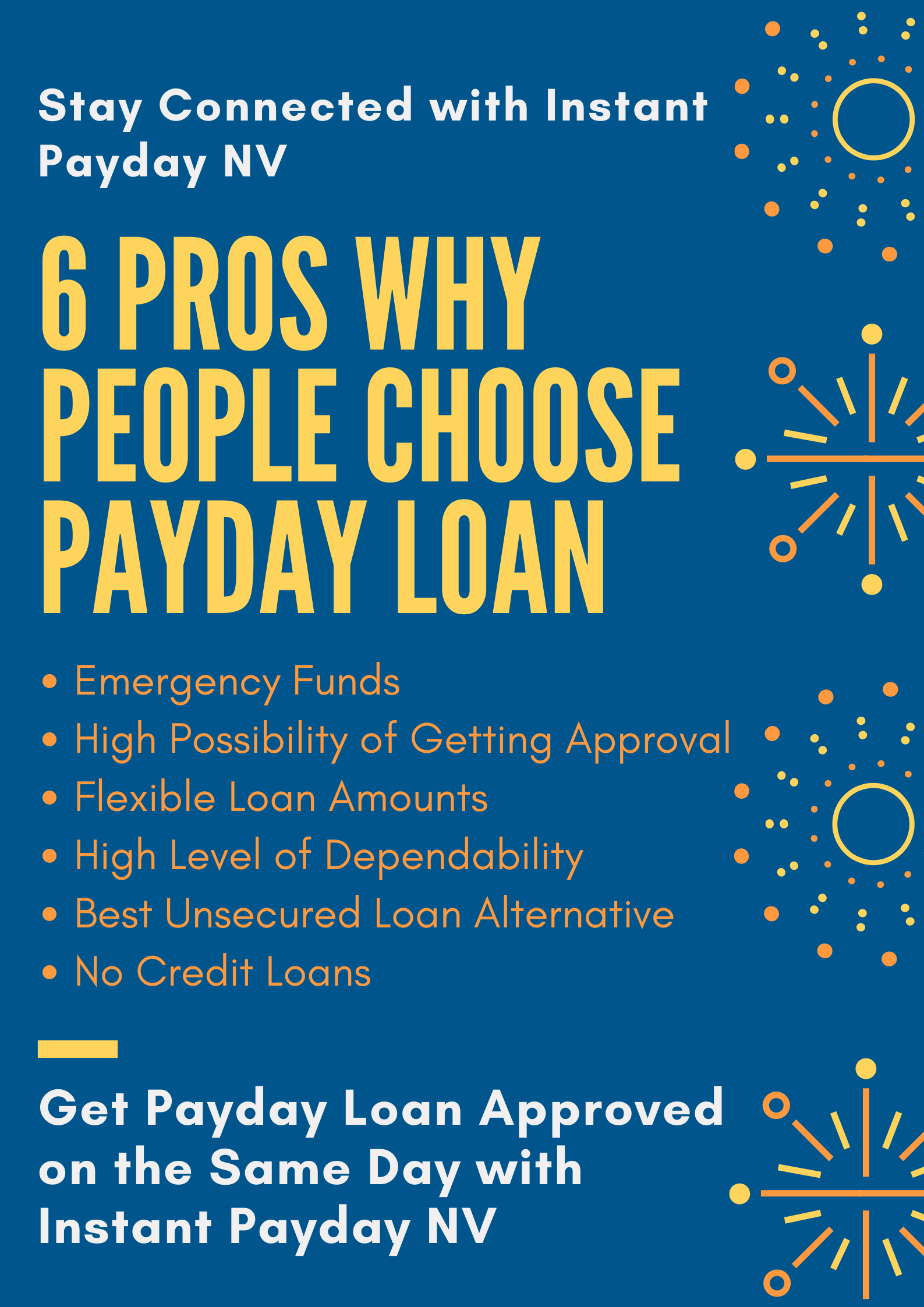

Below are the top 6 pros of online payday loans:

#1: Emergency Funds

In life, there’s no certainty – something must definitely come up that would require you to request for instant cash.

Yes – Emergencies do come up at some point (a friend may even need financial assistance for a pressing issue; your car may just break down, all of a sudden and will require quick repair).

Keeping that in mind, it’s encouraging to know that you can always access an online payday loan without having to wait for a long period of time.

And this’s one of the major pros of payday loans, and one of the reasons why people choose it over traditional bank loans and personal loans.

#2: High possibility of getting approved

There’s a high likelihood of you getting your loan request getting approved when applying via a payday lender.

First off, bad credit is one major factor that makes it really hard to find financial assistance when you need one.

But with a payday loan, you get a fair food chance of getting your payday loan request approved.

They are the best options for funding even with bad or poor credit.

#3: Flexible loan amounts

One very nice thing about payday loans is that they give you a variety of options of loan amounts to choose from – that is, you don’t always have to take out a large amount of money for something that ought to cost you less.

For example, let’s say that you have a pressing need worth about $300, unlike other traditional loans that would offer a standard amount of loan which could be way more than the amount of money you are in need of, let’s say $1000, payday loans offer flexible loan amounts that will coincide with the amount you need to cater for that your pressing need.

The best part?

Some payday lenders like Instant Payday NV actually offer funding that can reach up to $5000, which basically limits you to no amount of funding for your pressing needs.

But keep in mind that taking up payday loans of this amount comes with more stringent approval requirements, so ensure that you look into your lender’s specifics if you need a loan that’s as high as this.

#4: High level of dependability

Payday loans provide a high level of dependability to customers who are looking to supplement for their regular income.

This may be as a result of certain factors in one’s life that could constantly require them to be in need of instant cash on a moment’s notice.

#5: Best unsecured loan alternative

No payday lender will ask you to provide any form of collateral in order to qualify for the loan offer.

This is one of the main pros of payday loans – unlike regular traditional loans, mortgage or a car title loan, payday loans Las Vegas don’t require any form of security in the form of personal property.

That is, no payday lender is licensed to seize any of your personal property if you happen to default on a loan payment.

#6: No Credit Loans

Payday loans are no credit loans – that is, they don’t really consider your current credit rating or score in determining whether or not you qualify for the loan.

This also helps to prevent any other further damages on your current credit score, because, your inability to payback on a loan debt from a payday lender is not recorded in any of your credit history.

Since payday lenders do not pull your credit history, which also implies that there are no hard credit inquiries on a payday loan application request which could inadvertently lower your credit score by several points.

But you should also note that it’s also impossible to build on your credit score with a payday loan.

Finally, it’s important to note that, you might not get your payday loan request approved if you don’t show to your payday lender a clear way of you paying back the loan, with necessary proofs.

As a rule of thumb, the Consumer Financial Protection Bureau has an act that ensures that borrowers receiving payday loans are screened properly for their ability to pay back the loan debt.